Podcast: Play in new window | Download | Embed

Subscribe Apple Podcasts | Spotify | Android | iHeartRadio | Blubrry | Email | TuneIn | Deezer | RSS

Jan Kregel explains the fundamental problem with the economic system is its focus on providing finance to investors. Hyman Minsky, who understood that financial instability is inherent to capitalism, proposed changing the economy’s objective to employment.

Lynn Fries / GPEnewsdocs.com

TRANSCRIPT

JAN KREGEL: One of the things I think that people find very disconcerting in trying to interpret his work is that he has some very basic fundamental principles that he continues to use to analyze the capitalist system. But at the same time is always willing to stress that capitalism is a changing phenomena in which the changing financial structure has an impact on its performance.

And he was always very careful to identify the way institutions and that what he called the financial structure changed over time. And how this would change the way the system satisfied the basic requirements which he thought the capitalist system should produce. And that was to provide, or the financial structure should produce under capitalism, the financing of a reasonably stable productive structure in which it provided employment for the entire population and provided the possibility for maximizing the use of the available resources in the economy.

So this was always the thing which was at the back of his mind but the changes in the financial structure were something which were for him very, very, very, very important.

LYNN FRIES: Hello & welcome. I’m Lynn Fries producer of Global Political Economy or GPEnewsdocs. And that opening clip was from a commentary by Jan Kregel on the work of Hyman Minsky.

Minksy argued that the difficulty with capitalist governments is that their objective is simply economic growth by means of increased profitability that generates investment. And that by doing that, you create a financial system that itself produces crises. Minsky argued the way around that is to change the objective. That capitalist governments should have employment as their objective instead of growth by investment.

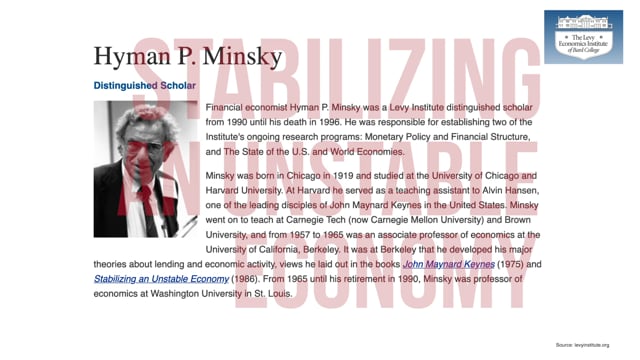

My guest, Jan Kregel is Director of Research at the Levy Economics Institute of Bard College and Heads the Institute’s ongoing research program in Monetary Policy and Financial Structure that Hyman Minsky was responsible for establishing.

Jan Kregel, welcome

JAN KREGEL: Pleased to be here.

FRIES: Jan, you recommend looking at the work of Hyman Minsky to understand crises under capitalism. The policy, for example, in the US government response in the 2007-2008 financial crisis and its aftermath, the Great Recession, you say moved in the opposite direction of what Minsky had prescribed -the rest is history, deepening unemployment and inequality. And that current COVID-19 crisis management is moving in the same direction and has devastating implications.

Jan, so we can all better understand crises under capitalism and a way forward take us through what you think are key takeaways from the work of Hyman Minsky. Like why just as the Federal Reserve acts as Lender of Last Resort to bail out too big and too interconnected to fail banks, the government should act as Employer of Last Resort to bail out households.

KREGEL: Well, Hy in the initial analysis of capitalism made the very astute representation that capitalism is a system in which the control and the operation of capital assets are determined by the ability to borrow to control those assets. So that it’s always the way the borrowing takes place in the system and the way the liabilities that are issued, in order to finance the acquisition of capital, [that] are crucial components of the ability of the system to produce full employment and to produce maximal well-being for the population.

So if we can simplify and say that under the postwar golden age period, you had a financial structure which was primarily set up to finance the acquisition of productive capital assets. Those productive capital assets then provided employment and they provided output.

Now that particular system Minsky criticized because its success required extremely high levels of investment in order to generate the growth in incomes that would produce increasing employment.

And the problem with this was what? Well, the problem was that the more liabilities you have to issue in order to finance capital equipment, the greater the instability that you produce in the system.

Now, where does that instability come from? Well, this is determined by one of these basic principles that Minsky used. And that was to look at the balance sheets of the various sectors of the economy: balance sheets of firms, balance sheets of households, balance sheetsof the government. These balance sheets always have assets and they have liabilities. So that if the system requires a very rapid increase in investment that means that it requires a very rapid increase in the issue of liabilities by the firms in order to finance those assets.

So if you ask the next question and say, where do those liabilities end up? The response is well they have to be financed. Who finances them? And you finance them by either borrowing from the banks or selling them to the public. So that this increase in existing liabilities is not only a problem for the firms, it also ends up linking the balance sheets of the banks and the balance sheets of households.

Now the risk comes from where? The risk comes from the fact that liabilities carry debt service requirements. You borrow money; you have to be able to pay it back. You either pay debt service in the form of interest or you pay debt service in the form of dividends.

So that the risk comes where? The risk comes in terms of the cash flows. That is the income that is generated by the investments, the capital assets, have to be sufficient in order to meet the debt service on the liabilities that you’ve issued. So that if your liabilities are going up more rapidly than the ability of your capital assets to generate income, it means that you may not be able to meet your debt service commitments.

In simple terms, you’re not able to meet your interest payments or the repayments of principle.

Now for the firms, this is a problem. This is a problem because we have legal principles which say that firms have to be able to meet their debt service commitments in order to stay solvent. Otherwise they enter into bankruptcy. But that’s just the problem for the firms.

The other problem is that the firms’ liabilities are now also on the balance sheets of the banks or the balance sheets of households. Who have either financed those liabilities in the case of the banks, giving the firms the money to purchase the capital assets; or the households using their savings in order to also purchase those liabilities.

So that if you have fragility in the firm sector, the firms are not able to meet their debt service, this automatically has an impact on the financial sector. The financial firms are expecting to receive interest payments and repayments of principle and they find that the firms can’t pay. So now it’s that the banks are in a condition of difficulty.

And the same thing then extends to households. So that if households have purchased say the bonds of IBM or AT&T and they’re unable to make those payments, now the households find that the value of their assets and their income is reduced.

So if we look at this interaction which is determined by the intersecting balance sheets -that is the assets and liabilities being held across the balance sheets of the firms, the banks, and the households -if it turns out that there is I would call this an excessive emphasis on investment in order to satisfy the conditions of employment and output growth, you have an increasing risk that firms will be unable to make those debt service payments.

If they can’t make those debt service payments, what happens? Well, first thing is they have to cut back on investment. Second thing, the banks find that they’re unable to continue lending. So they cut back their lending to the firms. And the households now discover that their income from these assets is reduced. So they stop spending.

And the result is what? The result is a reduction in investment spending, a reduction in consumption spending, a deficiency of aggregate demand and you start a crisis. And that crisis starts first as a recession.

The recession caused by what? Caused simply by the fact that investment is falling, consumption is falling and therefore output and employment are falling. If this becomes cumulative, you then end up with the possibility that Minsky called going into a debt depression or a debt servicing depression.

Why? Well, if it now comes to be the case that firms are unable to meet their debt service, they might in fact decide, in order to meet their commitments to the bank, to start selling their capital assets. So if they start selling their capital assets, then the price of capital assets goes down. And this generates then what Minsky called following Irving Fisher, a debt deflation process.

So that debt deflation process eventually ends up where? Well, it eventually ends up with widespread bankruptcies and the conditions that we saw in the 1930s in the Great Recession.

So that Hy’s basic idea was that if you look at these intersecting balance sheets and if you look at the balance between the cash inflows that you got from investment in capital assets relative to the cash commitments that you had in order to pay the liabilities, that is the debts that you had to issue in order to acquire those assets, there was a very high probability that the system would enter into frequent financial crises.

Simply because the emphasis on increasing growth and increasing investments would lead to this natural result of investments growing more rapidly than the ability of those investments to produce the debt service and to keep the economy stable. So this was basically his position up until around the period of the 1980s.

In the 1980s things in the US changed. And they changed relatively rapidly. They changed in a couple of different ways. The first way was the banks were no longer really interested in financing the acquisition of capital assets by firms. At the same time, firms no longer became very interested in producing income by purchasing capital assets. And bothof these sectors entered into what came to be called financial engineering.

Financial engineering meant what? Well, if you look from the point of view of firms: if you were the chief financial officer of the firm, instead of looking to find funding to buy capital assets, you now looked at the ways in which you could produce financial assets, not real assets; financial assets in order to create income. So that firms became concentrated on using the issuance of financial assets and the discrepancy in financial asset prices simply to generate incomes by trading financial assets.

Now there’s a very big difference between financing investments to produce real output and issuing financial assets simply in order to generate gains from basically what is mispricing in financial markets. Now banks started doing the same thing. That is banks started looking at the ability to create income by looking at mispricing in terms of financial assets.

This is what we call the difference between financing to get a gain on a price differential and financing in order to produce income that comes from operating say a printing press or an automobile factory. And what Minsky noted was that from the 1980s onwards, increasingly the financial system was concentrating on simply pricing differentials. Some people eventually called this financialization but basically Minsky talked about this as money manager capitalism.

Why? Because he said it now came to be the case that instead of managing assets in order to assess the profitability of real investments, that is, instead of looking at General Motors and saying does General Motors produce an automobile that is able to generate profits and are those profits sufficient to cover the cost of financing that is the debt service of those liabilities; now, the bankers are simply looking at the liabilities that General Motors issues and whether they can trade those liabilities in order to make a profit amongst themselves.

And this basically became what he called money manager capitalism. He said what happened is that money managers now would generate portfolios and they would manage those portfolios not in terms of the income that the portfolios generated, that is we’re talking about the income from sales of output, but generated income from their ability to trade those assets in order to take advantage of pricing differentials. So you have a very large increase in the liabilities that these banks are producing relative to the underlying basic productive structure.

Now, obviously very quickly after that I know you’re very familiar with the fact of the creation of hedge funds, the creation of private equity funds. All of these funds are created to do what? They’re all created not in order to finance the acquisition of physical capital assets that generate income. They’re all there in order to take advantage of price differentials.

So that Minsky said this had a very, very important impact on the way the system was going to operate. Why? Because now instead of having fragility of the system created by the net income generated by capital assets relative to the financing liabilities, the problem was the ability of all of these investment managers to generate a rate of return that was determined by their ability to trade.

All the investment managers or the money managers were then doing what? Well, basically they were competing against each other in order to generate the highest possible rates of return. And quite obviously as Minsky identified this meant that in order to generate these higher rates of return, it meant going into riskier and riskier types of investments.

Probably the best known example of this sort of risk was Long-Term Capital Management in the end of the 1990s. Long-Term Capital Management did not finance the acquisition of any real physical capital assets. All they did was to borrow and lend financial assets. Or we should say buy and sell financial assets in order to generate income from price differentials.

To do this because these price differentials are often times very, very slim (we’re talking about differentials between the bid and ask prices on the financial assets that they’re trading of 2,3 or 4 basis points [1 basis point is 1/100 of 1%]);it meant that on the trade you don’t make a great deal of money.

So that if you’re going to make money doing this, what do you have to do? Well, you have to go to scale. That is instead of buying and selling or selling one share, you buy a million shares. But to buy those million shares, you have to have capital. So you borrow from the banks, the capital in order to invest in these strategies of price differentials. So as Minsky rightly pointed out this meant a very substantial increase in risk.

Why? Because if it turned out that you guessed wrong on the way the prices were going to move and if you made a sufficiently large loss, then you wouldn’t be able to carry. That is be able to meet the debt service on the money that you borrowed. And you would then have to default on that borrowing. And the banks would then be in difficulty.

As I mentioned in Long-Term Capital Management, this is precisely what happened. Long-Term Capital Management had borrowed so much that when their strategies went wrong, that is when they guessed wrong and they lost money, they were unable to repay the banks.

Obviously we’re now back to the same position in which you’re creating a possibility not only of a recession but of a depression. Why? Well, if the banks stopped lending and the value of all these assets goes down, you have exactly the same process that we had before. But as you can see, the financial structure that produces the financial crisis is really very, very different.

This is just to give you an idea of two different financial structures that end up creating excessive financial liabilities relative to the possibility to service them. And a very small movement in expected values leads to a position in which people cannot make payments.

And when you cannot make payments, what do you do? You stop spending. And once you stop spending, then the economy goes into difficulty.

This basically gives you an idea of how Minsky used always this idea of looking at balance sheets, looking at the interconnectedness of balance sheets. But also looking at the financial structure as having a very determinate way of giving you an idea of where financial instability and where the possibility of recession and crisis came from.

Now, this is the basic reason why when Hy looked at alternative strategies for economic policy he came up with something which most economists considered as being very, very radical. Why? Well, obviously everybody believes that the economy is going to produce income and employment if it grows.

If it’s going to grow, it requires investment. But Minsky told us that if we had too much emphasis on investment, whether it was investment in real capital goods or in terms of financial assets, it was going to produce eventually a financial crisis.

Eventually Minsky turned out to be right. Because in 2007 and 2008, we did get the financial crisis which was determined basically by what? Well, this wasn’t a Long-Term Capital Management problem; this was the problem of the subprime mortgages.

Minsky said maybe we shouldn’t place so much emphasis on borrowing. Maybe we shouldn’t place so much emphasis on the necessity of financing either accumulation in real assets or the generation of these financial assets that we have under money manager capitalism.

So he said, really what we have to look at is the primary objective. And our primary objective is what? Well, normally our primary objective is either income or employment. And in this he goes back to Keynes’ General Theory where Keynes talked about the general theory of, and clearly there in the title you talk about, money and employment.

So Minsky said: let’s see if there’s a better way to get employment than simply financing investment and then hoping that the investment generates the profitability that creates the income and allows for the employment.

So his radical proposal was to say: really what we should be doing is selecting full employment as the objective for the economy. Okay. Now he had a very simple explanation for why this was important. Because he said: look, if you’re an economy that has a normal size and has a normal population, it will normally have a positive rate of population growth.

And that rate of population growth if you provide full employment will guarantee that the economy will grow at least at the rate that population is increasing. If you manage to have some technical progress at the same time, that is so that output per man is increasing, he said then by definition you know the economy is going to grow over time.

And if you have the emphasis on employment rather than the increase in liabilities, then you avoid the financial crises that comes with the risks that are created by the fact that in order to finance the expansion of the system, you have to increase liabilities in order to purchase the real capital assets as investment.

So his proposal was quite simply: let’s use full employment as the mechanism to do this. Now, he also recognized that it was probably not going to be the case that the private sector on its own would produce full employment.

There are all sorts of explanations for this. One of them is the one which was put forward by Kalecki that argued that private sector manufacturers would be very hesitant to allow the economy to go to full employment. Why? Well, because they believed that this would bring about a too rapid increase in wages. And this would cause a decrease in the profitability of the private sector.

Now was that a good thing or a bad thing? Well, if your objective is to increase the welfare of the entire population, it’s probably a good thing. And we talk now very much about the very rapid increase in income inequality and in terms of wealth inequality. And one of the reasons for that is precisely that wages have tended to be kept down either at or below productivity levels simply in order for profitability to increase.

So that the increase in profits and the failure to achieve full employment are obviously one of the basic causes of the very sharp increase in the share of income which goes to the top 1% of the income distribution. And the other part of this is the fact that most of the financing that we’re doing now is not financing employment, but is simply financing the acquisition of these financial assets. If you look at the argument about the money manager capitalism, money manager capitalism generates the kinds of incomes that in fact are the major proportion of the top point zero one percent [0.01%] of the income distribution.

Minsky argued: here’s a way for the government to come into the story. Minsky was very much influenced by the measures that were taken during the New Deal in order to stabilize income. And this meant spending income directly to provide employment. Okay. First thing that Roosevelt did was to create the Civilian Conservation Corps, send people out to plant trees. Producing what? Directly [producing] incomes for people who had been unemployed.

So from this Minsky got the idea that if you’re really worried about income inequality, if you’re really worried about unemployment and you’re worried about poverty, the most important thing is not to provide mechanisms, welfare mechanisms in order to supplement the incomes of people who don’t have employment. But it’s to give them employment directly.

And for this, he came up with what he called the Employer of Last Resort program or the Job Guarantee program. So that the other part of Minsky’s idea of shifting the objective from high investment and high growth to high employment was the requirement of the government to come in and directly provide employment.

Now, how was this different from the normal approach? Well, the normal approach is simply that if the economy is not producing full employment then the government should be spending. And it spends by increasing its expenditures relative to its tax yields or its tax income. Or increasing government debt, this is what basically we call debt financed expenditure. Now Minsky also, in a very coherent way, said probably this is not a very good idea.

Not a very good idea, why? Well, first of all, because it increases the amount of government debt outstanding. Now this may be a problem, it may not be a problem. Okay. But the point is that you really don’t need this kind of debt financed expenditures. Because government expenditures are usually across the board expenditures. Whereas unemployment is usually a relatively specific kind of unemployment.

A very interesting historical fact in the 1930s when Britain was recovering from the recession, Keynes’ disciples argued very strongly to increase debt financed government expenditures. And Keynes said, no. He said, I don’t think this is a good idea. And people said: well, maybe Keynes has become a non-Keynesian. He doesn’t believe in debt finance expenditures.

Keynes said no. That’s not the point. The point is that the unemployment that exists in Britain right now is, for example, in the shipbuilding industry. There is no possible way the ship building industry is ever going to recover no matter how much the government spends in terms of deficit financing.

Because Britain no longer has the economic structure and the global economy no longer has a set of international prices which will allow Britain ever to become a competitor in international shipbuilding. So he said government expenditures are useless. All they do is to increase incomes, but they don’t increase output and they don’t increase employment.

So the problem is that we have to be very careful. Yes, we want government debt financed expenditures. But we don’t want government debt financed expenditures that don’t have a net impact on output and employment.

And many people said: well in the General Theory Keynes talked about taking bank notes and burying them in the ground and that that was sufficient. Well, yes, there is a passage in the General Theory where Keynes says: if nothing else can be done, better to do that. Okay.

But then he goes on very quickly to say: but it would be much better if we used those funds to build hospitals and to provide overhead infrastructure services for the economy. So we’re back to Roosevelt and the CCC [Civilian Conservation Corps]. What did we do? Environment.

Roosevelt was very clear in the importance of taking care of the environment. So the CCC was probably one of the first environmental expenditure programs. And there’s absolutely no reason why these programs can’t be used in order to provide employment that the private sector doesn’t.

Minsky’s proposal was that not only do you need the objective for the economy to be full employment but you have to be willing to structure your economic policy in order to ensure that particular objective.

And some sort of employer government job guarantee program, Employer of Last Resort program will be necessary. And it’s also necessary to tailor that program so that it does support the ability of the economy to maximize the use of its particular resources.

FRIES: We have to leave it there. Many thanks to Jan Kregel who joined us from New York. And from Geneva, Switzerland thank you for joining us in this episode of GPEnewsdocs featuring a commentary of the work of Hyman Minsky by his colleague and friend, Jan Kregel.

END TRANSCRIPT

Jan Kregel is director of research at the Levy Economics Institute, director of the Levy Institute master’s program in economic theory and policy, and head of the Institute’s Monetary Policy and Financial Structure program. He also holds the position of professor of development finance at Tallinn University of Technology. In 2009, Kregel served as Rapporteur of the President of the UN General Assembly’s Commission on Reform of the International Financial System. He previously directed the Policy Analysis and Development Branch of the UN Financing for Development Office and was deputy secretary of the UN Committee of Experts on International Cooperation in Tax Matters. His major works include a series of books on economic theory, among them, Rate of Profit, Distribution and Growth: Two Views (1971); The Theory of Economic Growth (1972); Theory of Capital (1976); and Origini e sviluppo dei mercati finanziari (1996).