Similar Posts

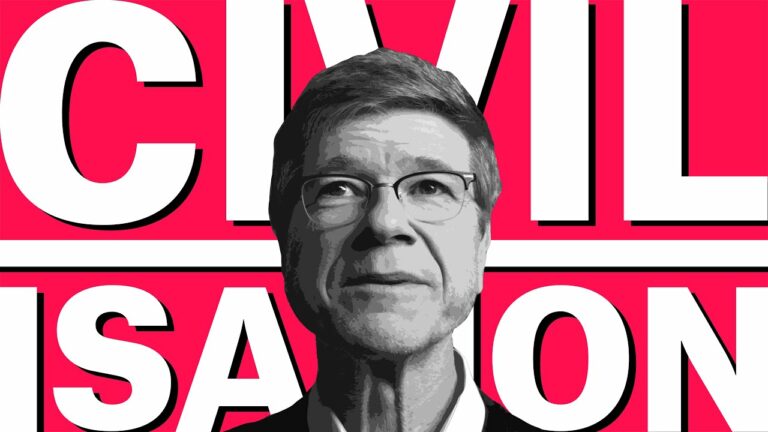

America Vs. Everyone – Jeff Sachs

Jeff Sachs talks with Rob Johnson about the tragedy of modern geopolitics, and how our current race to the bottom could be reversed. This is an interview taken from the Institute of New Economic Thinking. For more of their material, please visit ineteconomics.org.

Warfare State at War with Trump as He Plans Warfare Against Iran – RAI with Norman Solomon (pt 2/4)

This is an episode of Reality Asserts Itself, produced on May 22, 2017. Norman Solomon joins Paul Jay on Reality Asserts Itself, discussing the Trump/Russia affair and plans to isolate and perhaps attack Iran.

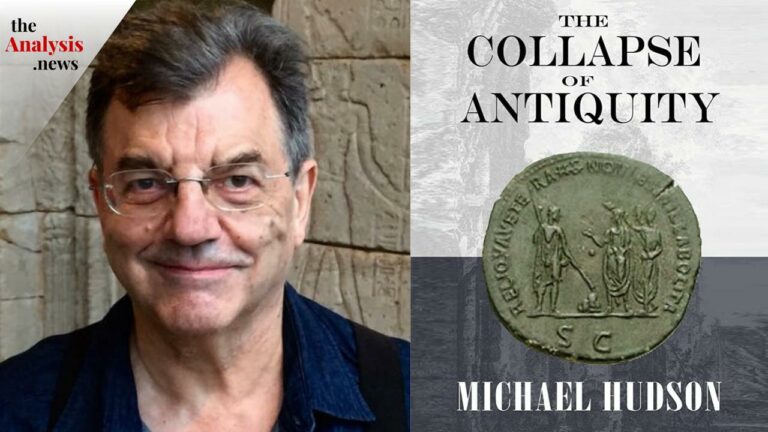

Part 2: Debt and the Collapse of Antiquity – Michael Hudson

In part two, Michael Hudson discusses his new book “The Collapse of Antiquity.” Hudson challenges the traditional beliefs about the fall of the Roman Empire, arguing that it was caused by a financial crisis brought on by excessive debt, wealth inequality, and the concentration of economic power. Hudson draws parallels to modern-day economies and highlights the dangers of financialization and wealth concentration.

Project 2025 Will Decapitate Civilian Oversight of the U.S. Military – Mikey Weinstein

The First Amendment guarantees religious freedom and the separation of Church and State, basic tenets of American democracy which conservative think-tank the Heritage Foundation is intent on undermining. Mikey Weinstein,…

The Significance of the “Shit Show” Debate – Panitch, Day, Horne & Jay

Prof. Leo Panitch, Jacobin writer Meagan Day, and Historian Gerald Horne join Paul Jay to analyze the Presidential debate and the underlying reasons why the U.S. political system is in disarray. They discuss how the people’s movement will respond to a possible Trump coup if he loses the election.

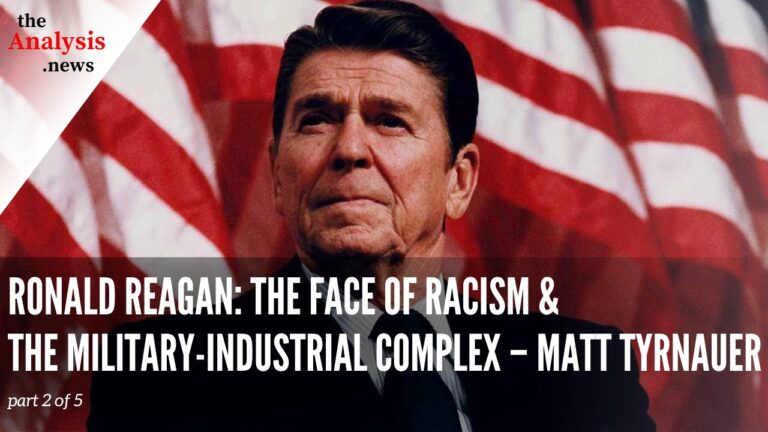

Ronald Reagan: The Face of Racism & the Military-Industrial Complex – Matt Tyrnauer (pt 2/5)

Reagan understood the American psyche from within it. He used his acting skills to sell right-wing “dog whistles” and militarism. Matt Tyrnauer, director of “The Reagans”, on theAnalysis.news with Paul Jay. This interview was originally published on January 29, 2021.

I suggest Mr Ferguson reread Mike Moore’s Stupid White Men on Bill Clinton being the best or worst republican POTUS America never voted for, before trying to alibi the duplicitous , absolutely corrupt , and perhaps senile Joe Biden as Americas white knight.

Voting is of little importance and has been since our defeat in Vietnam , when CIA and the the various deep state entities controlled by unelected elites decided that guys like Carter , Nixon , and Kennedy were unreliable and began openly fixing the results. These days the SCOTUS, and Electoral College are the primary tools , supplemented by electronic ballot rigging , voter suppression , and gerrymandering of districts . Whether Trump or Biden sit on the now mainly ceremonial POTUS throne is truly immaterial to the global elites that now rule most of the planet.

The characterization of today’s (since 2009) QEs as “Keynesian” stimulus is incorrect. If JM Keynes were alive today, he would be vociferously denouncing the Fed and the Treasury as irresponsible. Keynes, in his 1936 treatise, “The General Theory of Employment, Interest, and Money”, urge federal borrowing when there is growth stagnation and high unemployment. Its object was the stimulation of aggregate demand by putting people back to work. Keynes saw this as the singular responsibility of the federal government, because private investment in times of GDP stagnation is discouraged by the wide perception of unacceptable risk. Only the federal government can provide the needed employment stimulus . This is very different from increasing the reserves of the major banks so that they and their privileged borrowing corporations can help themselves in the stock market rather than invest and increase employment. That is not Keynesian stimulus.

I can think of no person who was and is still detested as much as FDR by his own capitalist class as was JM Keynes. If Keynes had been in charge at the Bretton Woods conference in place of Harry Dexter White, an agreement could have been made that might have avoided the domination of the postwar economy by the US and the ultimate breakdown of the gold standard (1971). If Keynes had been heard after WWI, the Versailles Treaty would not have set the stage for WWII. He was a profoundly far sighted political economist and one of the key intellectuals of the 20th century, as recognized and celebrated by Bertrand Russell in his “History of Western Philosophy”.

Great post I heartily agree.