The problem of inequality won’t be solved simply by more education and training; inequality is hardwired into the rules of this hyper globalized world. The director of the Division on Globalization and Development Strategies at UNCTAD joins Paul Jay on theAnalysis.news podcast.

Transcript edited for clarity.

Paul Jay

Hi, I’m Paul Jay. Welcome to theAnalysis.news podcast. Don’t forget there’s a donate button

at the top of the webpage.

This is part three of my discussion with Richard Kozul-Wright, who’s the director of the

Division on Globalization and Development Strategies at UNCTAD, the United Nations

Conference on Trade and Development. He’s the author of the 2020 Report of UNCTAD

‘Transforming Economies: Making Industrial Policy Work for Growth, Jobs, and

Development’.

You really should listen to Part One and Part Two, because it will make a lot more sense if

you do. But it will still make sense, I think, even if you don’t.

So before I introduce and say hi to Richard, I’m going to read a quote from the report. So this

is in the chapter ‘Almost Everyone Left Behind.’

“In a textbook world, income distribution is a well-rehearsed fiction. Wages are negotiated in

markets where everyone has equal bargaining power, and the outcome is a wage reflecting

each worker’s productivity. Only in this narrow sense is the income distribution fair. In the

real hyper globalized world of austerity and depressed employment, corporations wield

unique power in wage negotiations, and the textbook foundations of fairness and distribution

melt away. Even so, any rising inequality from more liberalizations is justified, assuming that

the gains from improved allocation of resources, empowered middle-class consumers, and

improved government revenues would be more than enough to compensate those at the

bottom. That conclusion requires dubious assumptions like full employment everywhere and

at all times. It also misses the point. Power and policies, not fair competition, determine how

adjustment processes play out.”

So thanks for joining us, Richard.

Richard Kozul-Wright

Nice to be back, Paul.

Paul Jay

So break that down. When you call this fair negotiations, and they keep talking about a fair

wage, it’s almost like fair taxes, that it’s a well-rehearsed fiction. Why do you call it so?

Richard Kozul-Wright

It’s one of the great weaknesses of conventional economics, its inability to deal with the

distribution question in any serious way, and to offer what is ultimately just a justification for

the status quo. That’s a longstanding debate and a critique of most heterodox economists.

Paul Jay

What is that?

Richard Kozul-Wright

Anyone who is outside of the kind of mainstream neoclassical tradition, based on these

ideas that the economic activity is simply a set of transactions between individuals who have

are fully rational and fully endowed with all the necessary information to make optimal

decisions. As long as markets are left alone and not interfered with by governments, then

prices will allocate resources in the most efficient way, and everyone will be happy. I mean

anyone who recognizes that as a kind of mythical view of capitalist economies, it’s in one

way or another heterodox, and it’s a broad group that encompasses everybody from both

post Keynesians through the Austrians and Marxists, to be quite honest. But it’s a rejection

of that very stylized view of optimal market behavior.

Paul Jay

OK, well, keep breaking down then. So explain why that’s fiction, and how does it affect

people?

Richard Kozul-Wright

I mean, for the reasons we said in terms of power, if you take power out of the transactional

relationship between buyers and consumers and producers, between creditors and debtors

and of course, between labor and capital, you’re going to take out one of the most important

elements of both of those relationships. In our world, everyone recognizes that inequality has

increased massively over the last three decades, four decades, everywhere.

No one disputes that. I think there are different attempts to understand why that’s taking

place. Amongst many economists, it’s a debate about whether trade or technological change

has been the source of these growing inequalities. Behind that is this idea that trade and

technology are good, but somehow certain groups of people have been forgotten about or

left behind; that is the kind of phrase that reverberates around our world to explain the

growing disparities within and across countries.

This idea that we forgot about people and all we need to do is just give them a bit more

education or train them a bit better, and everything will be all right. That we want to critique

the analysis that we’ve been doing now for some years and to remind people the inequality

is hardwired into the rules of this hyper globalized world. It’s a very footloose capital and

increasingly flexible and precarious labor market conditions and policies that are oriented

towards maintaining the place of those at the top of the pile.

It’s not a kind of accident that we see this growing inequality. It’s how the system works. It’s

how the system is intended to work. There are these very increasingly large semi

monopolistic or monopolistic corporations with a huge amount of economic-political power in

the position to generate rents for themselves. Rents rise to the top. Wages are kept down as

labor market institutions and regulations are eviscerated. So wages stagnate, and kind of

desperation happens. The one thing that trickles down in that world is desperation,

essentially. That kind of recognition that it’s the rules of the game and not a kind of accident

or forgetfulness that has created the kinds of inequalities that we see. It is kind of central to

the work that we’re doing.

Paul Jay

And desperation is very profitable. I know when I lived in Baltimore, I keep citing this

example, but I think it’s a good one. It’s kind of typical what was going on there. There’s such

high unemployment in Baltimore that people were desperate for jobs. So we talked to a guy

at Johns Hopkins Hospital who had 14 years seniority, cleaned surgical rooms after, had to

clean up the blood and guts, risking infection, had to take special drugs to try to avoid getting

infected. At the time, we talked to the guy; it was maybe two-three years ago, he was making

13 dollars an hour.

It’s only possible to get such cheap labor if people are so desperate. You can look at that on

a global scale, and then you talk about footloose capital, the fact that big corporations can go

where the labor is cheapest, play countries off against each other to some extent. To some

extent, they need a ‘China’ that has a disciplined work and trained workforce. But even there,

the Chinese government for a long time was helping keep wages low, maybe a little less so

now. But for a long time, they were.

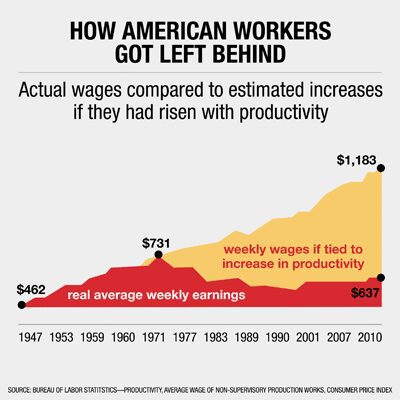

You have a situation wherein your report you talk about how the share of income that goes

to profits has been going up and up in relationship to wages. But I think you make a very

important point about the moment we’re in, which is all of this existed pre-pandemic.

You write, “if these pre-COVID-19 forces of wage repression remain in place, the labor share

will likely continue its decline in many economies in the next years, exacerbating inequalities

in the United States. After a 50 year dissent, the labor share is now back to its 1950s level. If

current trends continue in 10 years’ time, it will be back to the brink of the abyss level of

1930″. One should add to that with this massive unemployment; there is no way wages are

going up. The only way they’re gone is down.

Richard Kozul-Wright

In a way, there’s even more to that story. Particularly at the top, there’s a tendency to ignore

the nature of economic power at the top of the tree. A lot of that increase profit goes to very

large international corporations. There are much smaller and more precarious businesses

that do not benefit in the same way. You watch how these large firms operate. Not only are

they in a position to generate very large rents through intellectual property and control over

brands and monopsony power and other mechanisms, but of course, they’re in the position

to hide those profits from governments. Effective tax rates are extremely low as a

consequence, forcing governments into borrowing and problems that emerge in the balance

sheets of governments.

Not only do they hide the profits in tax havens, despite the fact that people have this image

of tax havens as somehow being kind of Caribbean islands or fancy guys in Panama shirts

parading on beaches. Most of the big tax havens in this world are in the advanced

economies. But these companies are able to shift profits around these tax havens to hide

their profits.

What do they do with their liquid resources? They don’t invest in productive activities:

investment and skills; they buy back their own shares, which has been taking place on a

phenomenal scale since the end of the global financial crisis.

The figure I saw, S&P 500 companies have channeled a trillion dollars a year into share

buybacks as part of the financing themselves.

Paul Jay

Interestingly enough, accumulating almost the exact same amount of corporate debt, about

a trillion dollars.

Richard Kozul-Wright

Yeah, because it’s more profitable to borrow and invest in financial assets than there is in

your own kind of productive activity, because who are you going to sell this stuff too. As

wages are repressed, demand is kept low, and the returns on investment in those activities

become minimal. The best way to make money is to engage in short term financial

transactions of one kind or another. These big corporations are sitting on piles of liquid

assets that they use for those purposes.

Paul Jay

You write, “A sustainable recovery requires faster wage growth for low wage jobs, too, in

order to revive productivity and employment growth, wage repression and ever weaker labor

market rules are only going to make the world economies pre-existing conditions worse.”

And it’s interesting when they had this CARE legislation which gave some money to people

during the pandemic, which is far from over. As we talk, they supposedly are going to start

negotiating again for a package in the Congress, although it looks like it’s not really going to

happen.

But the Republicans, one of the things they’re most concerned about is that some people

were getting more subsidy than they were getting wages when they were working and how

horrible that was that people might get used to that kind of money and demand higher

wages.

Well, actually, that’s precisely what is needed. But everything they do is in the other

direction. They see such a direct connection that if you pay higher wages, your profits are

not as high and the same thing globally. How they think a world, much of which is going to

be devastated by the pandemic, is going to somehow also be a market for goods. Most

Americans just don’t care about any market outside the United States. The bottom line is

that it’s simply not rational.

Richard Kozul-Wright

This is where we try and link in the notion. Everyone’s now talking about recovering better or

building back better. Is that Bidens’ slogan?

Paul Jay

Yeah, something like that.

Richard Kozul-Wright

Building back better. Our solution to that is an expansionary macroeconomic agenda

focused on full employment with an appropriate mix of monetary expansionary/monetary

policy, very importantly, a fiscal policy and public investment. But that’s not the end of the

story. Clearly, if you’re going to recover better, if we’re not going to repeat the mistakes of

the past 2009 financial crisis, we need this kind of New Deal agenda. Our reading of the old

New Deal was that it was a combination of, first of all, relief, then recovery and then

redistribution and regulation, particularly the regulation of finance. The redistribution was all

about strengthening organized labor in one way or another and building a middle-class on

the basis of this. I listened to Biden in the debate, and his inability to defend the idea of a

Green New Deal is quite shocking because it was the old New Deal that precisely made the

middle-class great in America the first time around.

The inability to make that connection with the kinds of policies that are needed post-COVID-

19 was pretty sad, really. That kind of combination of recovery and redistribution and

reregulation is the heart of the alternative that we want to say is not only relevant in the

United States or Western Europe, but also in many developing countries.

Paul Jay

The reluctance of Biden to talk about a new deal in that way, people try to say it is because

he doesn’t want to alienate centrist voters and Republicans who might come over to the

Democrats. And maybe there’s a minor factor in that. But I think it’s far more he doesn’t want

to alienate the financial sector, because right now, I think a good part of the financial sector,

maybe even the majority, are OK with Biden being president.

I think they would like to see a Republican Senate so they can control anything that actually

gets done. But I think they realize Trump is enough of a madman that they’d rather have a

more reliable neo-liberal politician running the state. That puts a lot of pressure on Biden, not

to talk about something that sounds too much like a New Deal.

I once asked Tom Ferguson, who is a political economist, he knows a lot of the people in the

finance sector, what he thought, how they would react to a Bernie Sanders or Warren versus

fascism if that were their choice. Like Trumpient real authoritarianism or a Warren or a

Sanders. He said they would choose authoritarianism if a wealth tax were on the table, that

to them is simply unacceptable.

That’s part of an outlook and pressure that’s on Biden for staying within the realm of what the

financial sector will accept, which I guess is also a reflection that sort of a people’s

movement pushing from the other direction isn’t strong enough right now.

Richard Kozul-Wright

Yeah, I guess. That’s probably true. That’s not an exclusively United States problem. That

rejection of the New Deal begins with Clinton, if not before. This point that we want to try and

make is that those kinds of measures were the basis in which you got an expanding middle-

class.

It’s true of Western Europe, although we didn’t call it a New Deal, but similar types of policies

that focused on full employment in which wages were in some way connected to productivity

improvements because of the strength of organized labor. Because of that, firms were forced

to kind of innovate and invest rather than channel their profits into financial activities of one

kind. You get this kind of virtuous circle in the 1950s and 60s across advanced capitalist

economies, which was the basis of a growing middle-class. Given the way in which we’ve

seen the wage decline consistently over 40 or 50 years, underneath that politically,

sociologically is this evisceration of the middle-class. ‘The Vanishing of the Middle-Class,’ I

think, was the title of a book by Peter Temin. That’s what you see. You would have thought

progressive politicians would want to hold that up as an alternative to what we’ve seen over

the course of the last 30 or 40 years and the kind of anxieties and frustrations that has bred.

Paul Jay

Well, you in your report say it, if they don’t take the kind of approach you’re suggesting, you

call it a doomsday scenario. So in the next segment of our interview, we’ll talk about your

recommendations for what you think should be done. And also, I’m going to raise the

question, shouldn’t more public ownership be part of those recommendations? But we’ll do

that in part four of our conversation.

So thanks very much for joining us, Richard.

Richard Kozul-Wright

Thanks, Paul. Thanks for the invitation.

Paul Jay

And thank you for joining us on theAnalysis.news podcast.